Y Combinator: The Institute of Innovation

YC has more weapons than any other player in venture.

If you only have a couple of minutes to spare, here's what investors, operators, and founders should know about Y Combinator.

- Full stack venture. YC is best-known for offering a three-month program for new entrepreneurs. That mental model is outmoded. The organization founded by Paul Graham now helps from inception through pre-IPO.

- Network effects. YC is a venture capital firm with network effects. By batching its portfolio into cohorts and connecting them through internal tools like “Bookface,” it has created a structure that becomes stronger as it scales.

- Pricing power. As venture capital has become more competitive, valuations have risen. Not so at YC. The accelerator manages to invest in startups at a significant discount that has increased relative to the market over the past decade.

- Matters of diversity. Compared to industry benchmarks, YC invests in more women, black, and Latinx-founded businesses – but its numbers have stagnated in recent years. Many feel YC could do more to increase its share of underrepresented founders.

- A global presence. Just 49% of startups in the latest YC batch came from the United States. As more pre-seed and seed funds have come to market in America, YC has found success attracting promising entrepreneurs from countries like India, Mexico, and Nigeria. One nation that YC hasn’t cracked? China.

Y Combinator has more weapons than any other player in venture capital. No one else has such pronounced network effects, pricing power, and brand equity wrapped up in a single package. Perhaps that’s because YC isn’t really a VC firm – at least, not a traditional one. Depending on how you parse it, you can make a case that it’s any one of these five things:

- A university that treats companies, not people, as the atomic unit

- A startup that monetizes through an uncapped income share agreement

- A for-profit college that scales (and is not a scam)

- A social network for some of the world’s best entrepreneurs

- An industrialized venture firm

With a bit of stretching, you might be able to conjure half a dozen other reasonable descriptors. This amalgamation of ideas may be part of the reason that, nearly two decades after it was founded, the tech industry doesn’t seem to be sure what to make of YC. Some think of it as entrepreneurship’s Ivy League, the institution responsible for catalyzing a wave of innovation that has changed the world for the better. For others, it’s an apex predator, inflicting harsh terms on naive founders.

Underlying either position is the understanding that Y Combinator is extremely powerful. It does not seem hyperbolic to suggest it may be among the most consequential entities across industries of the last twenty years. Not only did YC support Airbnb, Stripe, Coinbase, DoorDash, Flexport, Rappi, Reddit, Vanta, and many others, it popularized a now-ubiquitous philosophy of company building. “Make something people want,” “do things that don’t scale,” and “getting to default alive” are gospels that owe their proliferation to YC. Over time, it has turned its success into a series of compounding advantages that make it look very different than anyone else in the market.

In today’s piece, we’ll chart Y Combinator’s history and evolution and navigate the debates that surround it. Read on to learn about:

- Origins. Paul Graham, Robert Morris, Trevor Blackwell, and Jessica Livingston founded YC in 2005. Their new creation relied on four powerful, non-consensus beliefs.

- Product. YC has developed an arsenal of tools to help startups at each phase of their life. That includes programs like Startup School and Work for a Startup, as well as tools like Bookface and Hacker News.

- Investing. President Geoff Ralston wants YC to be helping tens of thousands of startups a year. At its current growth rate, how long would it take YC to reach such figures? We crunched the data to find out and better understand how the firm’s investing has evolved.

- Terms. Are YC’s terms fair? Seven percent for $125,000 represents a discount from median pre-seed and seed valuations. Supporters believe YC makes up for it elsewhere.

- Risks. Accelerators like Entrepreneur First, Hyper, and Pioneer have found different ways to compete for early-stage investments. Now, megafunds like Sequoia and a16z are entering the ring.

Let’s get to it.

Origins: Fierce nerds

In 2005, a convict, a painter, a marketer, and a Canadian decided to start a venture capital firm. Over the next seventeen years, it would transform from a small summer program into one of the industry’s most powerful organizations, backing 3,000 startups and creating a combined value of over $600 billion.

Hackers

It had been seven years since Paul Graham, Trevor Blackwell, and Robert Tappan Morris had sold their company Viaweb to Yahoo in an all-stock deal valued at $49 million. That represented a life-changing outcome for the firm’s founders.

They had made an eclectic team. Robert Tappan Morris was certainly the most notorious of the executives. After getting kicked out of Harvard for reconnecting the university to the ARPANET, Morris had migrated to Cornell and set about coding one of the internet’s first pieces of malware. Borne of curiosity, the “Morris worm” spread to Harvard, Princeton, Stanford, and NASA. Some estimates suggest it impacted 10% of the 60,000 computers connected to the internet, though that estimate has been disputed. There was more than a bit of irony in Morris’s authorship. The worm took advantage of a vulnerability in a “sendmail” program running on Unix, an operating system Morris’s father had contributed to creating. At the same time that Morris Jr. was charged under the Computer Fraud and Abuse Act – the first person in history – Morris Sr. was working at the National Security Agency. The younger Morris was subsequently fined, sentenced to community service, and put on a three-year probation.

Morris’ inquisitiveness might have gotten him into trouble, but there was little doubting his genius. Among his admirers was friend Paul Graham. Graham shared Morris’s love of programming but married it with a serious interest in the arts, following a Harvard Ph.D. in computer science by studying painting at the Rhode Island School of Design (RISD) and Florence’s Accademia di Belle Arti.

Viaweb’s third cofounder arrived after Graham and Morris had broken ground on Viaweb. The idea was to build the world’s first “web app,” though that nomenclature had yet to emerge. Functionally, Viaweb allowed businesses to make and host online stores. This was a radical proposition at the time. Though Morris could “program as fast as he could type,” according to Graham – a description he qualified by noting it was in C – more firepower was needed. When Graham asked Morris who the smartest person he knew in grad school was, Morris replied: Trevor Blackwell.

That recommendation surprised Graham; he considered the Saskatoon-native to be something of a “goofball.” As he would discover, Blackwell was “one of those people who’s a lot smarter than he seems,” blessed with prodigious programming ability.

In 1998, three years after its founding, Yahoo purchased Viaweb, later using it as the basis for Yahoo Shopping. One of Graham and Blackwell’s first acts once the deal had been finalized was to march Morris to a piercing studio. He had promised Graham that if Viaweb ever made him a millionaire, he would get one of his ears pierced. Viaweb’s sale had done that and more.

Batch 1

Seven years had given ample time for the perforations to heal over and the thrill of financial freedom to subside. One afternoon in March of 2005, Graham emailed his old cofounders to try and find something new to work on. As it turned out, they would not have to wait long to find a new challenge. The impetus for it came from outside their trio.

If Graham, Morris, and Blackwell had already landed a big hit, Jessica Livingston was still looking for hers. Raised in Boston by her grandmother and single father, Livingston had a peripatetic start to her career, working as a customer service agent at Fidelity before moving to Food & Wine magazine. Stints in wedding planning and an “automotive consulting group” led to a marketing role at Adams Harkness, a boutique investment bank. It was while working at the firm that Livingston was invited to a party at Paul Graham’s house. The pair quickly hit it off and began dating.

As Livingston learned more about the startup world through Graham, she became increasingly interested and decided to apply for a job at a venture capital firm. True to the stereotype, the firm dallied en route to a decision, giving Livingston and Graham time to reflect on the inadequacies of the current venture model. Discussing the subject on a walk one evening, Graham was struck with an idea: rather than Livingston trying to reform VC from the inside, why not simply start a firm of their own?

By the time they got home, Graham had agreed to invest $100,000 in a new entity, helmed by Livingston. In the days that followed, Morris and Blackwell decided to join as partners, putting $50,000 each into what was initially named “Cambridge Seed.” Recognizing the geographical limitations the name implied, the quartet quickly moved to a more expansive if wonkish moniker: Y Combinator.

None of YC’s founders had ever been venture capitalists before. To learn as quickly as possible, they landed on the idea to fund a “batch” of companies, all at once. Rather than learning from ten startups stretched over an investment period of three years, they’d follow that many over just three months.

That summer, YC welcomed its first entrepreneurs to its “Summer Founders Program.” Described as a “summer job, except that instead of salary we give you seed funding,” Graham expected little financial return from the inaugural batch. As it turned out, YC’s founding quartet was gifted at attracting and identifying talent. Graham has noted that Livingston was particularly influential on this front. Nicknamed “social radar,” Livingston had an intuitive sense of founder character that complimented the three programmers’ technical analyses.

In hindsight, many of YC’s core innovations were visible in this first class. The firm took four non-consensus positions:

- Investing terms needed to be standardized. Seed funding was immature when YC got started. As a result, there were no benchmarks for typical deal terms. Founders often cobbled together cash from family and friends. YC decided to standardize the process by offering $20,000 for roughly 6% equity.

- Entrepreneurship is teachable. Innovation is often depicted as resulting from a single stroke of genius rather than a concerted process. YC’s curriculum challenged this notion by teaching new founders how to build a business, step by step.

- Hackers make for better founders than suits. YC is optimized for a different kind of entrepreneur. Rather than pursuing grey-haired executives ready to leave the bower of big business, it sought technologically-gifted youngsters. Over the next two decades, this would become the prototypical profile for tech entrepreneurs.

- Startups can be funded synchronously. Venture capital firms traditionally funded companies one at a time. By experimenting with funding ten businesses at once, YC uncovered a crucial lesson: connecting early-stage entrepreneurs to one another is extremely valuable. This marked the beginning of YC’s network effects.

Reddit proved to be the breakout winner of the batch, though it took some time for it to fully play out. Several other startups, including Parakey and TextPayMe, were acquired.

On an individual level, the caliber of talent assembled was extremely impressive. YC’s summer 2005 batch (abbreviated to “S05”) included Sam Altman, Alexis Ohanian, Steve Huffman, Aaron Schwartz, Brett Gibson, Blake Ross, Joe Hewitt, Emmett Shear, and Justin Kan. Outside of Reddit, that constellation has been involved with the creation of companies and funds including Twitch, Firefox, Initialized Capital, Seven Seven Six, and OpenAI.

In the black

By the time it ran its second program, YC had moved to Mountain View, California. Over the next few years, the firm continued to hone its curriculum. Funding for companies like Airbnb, Stripe, Dropbox, and Mixpanel came from Graham, Morris, and Blackwell’s balance sheets.

Daniel Ha, who attended the accelerator in the summer of 2007, described the early atmosphere as convivial and casual. “Back then it was more like an after-school program,” he said. “They kind of winged it along the way.”

Much of the program’s day-to-day relied on Livingston’s efforts, Ha recalled. “She was the heart,” he said, “She ran everything.” Graham served as a font of wisdom. Ha described listening to Graham speak and wanting to “mentally bookmark” everything YC’s founder said. “He had this weird mix of extremely approachable and intimidating,” Ha noted. “Things he said back then when I was twenty years old are things I still cite now.” Ha’s company, Disqus, raised funding from Union Square Ventures and Felicis before selling for $90 million in 2017.

Just a few months later, Adam Wiggins matriculated to Y Combinator along with his cofounders. Their company, Heroku, would prove to be especially significant to the accelerator.

Like Ha, Wiggins valued the advice YC’s partners and extended network provided. Highlights included Graham’s opening monologue imploring the cohort to “quit your other jobs” and focus during the program. Evan Williams, then building Twitter, gave a talk on the importance of “not trying to solve every problem,” a lesson he had learned the hard way while running Blogger. Marc Andreessen also visited, sharing his excitement about his social media network, Ning. (“A good reminder that even brilliant entrepreneurs with multiple hits still make bets that turn out to be wrong,” Wiggins said.)

Wiggins also benefited from connecting with batchmates, “Being around others going through the same struggles was an incredible boon for weathering the tough times.” Wiggins leaned on this network when Heroku received an acquisition offer, asking active and exited founders how they had handled similar circumstances and what the personal impact had been.

In late-2010, Salesforce announced its acquisition of Heroku for $212 million in cash. Not only was that a transformational outcome for Wiggins and his partners, but it also proved a milestone for its funder. For six years, Y Combinator had operated at a loss – Heroku’s sale pushed it into the black.

By that point, YC had taken its first outside funding. In 2009, Sequoia Capital invested $2 million in the firm with participation from future partners Paul Buchheit and Geoff Ralston. Limited partners (LPs) never seemed to be in short supply after that point. Sequoia re-upped in 2010, investing a further $8.25 million. Less than a year later, YC founders began receiving an additional $150,000 as standard, though the capital came from outsiders. Yuri Milner and Ron Conway’s Start Fund indexed the batch and gave entrepreneurs more runway.

In the following decade, Y Combinator scaled the capital at its disposal and the number of businesses it funded. We’ll investigate how the firm’s investing volume and mix have changed. First, let’s examine how Y Combinator innovated on the fundamental product of venture capital.

Product: Going end-to-end

“YC is no longer just an accelerator,” said Anu Hariharan, “It’s a full stack product.”

Coming from the Managing Partner of YC’s growth-stage vehicle Continuity, that description feels particularly apt. Look at YC today, and you’ll find a firm designed to support entrepreneurs from pre-idea through pre-IPO. Let’s take a look at what they’re offering at each stage.

Pre-idea

YC’s product begins at the pre-idea phase. Earlier this year, YC announced it was bringing back “Startup School,” a free, seven-week online course taught by partners and former founders. Though the first iteration of Startup School had an application process and focused on current entrepreneurs, YC has now made the curriculum free and provided a path for “aspiring founders.” Local meet-ups are being held in nearly thirty cities around the world, from São Paulo to Singapore. Entrepreneurs can also connect through an online portal. Previous class sizes have topped 40,000.

In July 2021, YC launched another product geared towards this stage: cofounder matching. After filling out a profile, would-be entrepreneurs can connect with cofounders tailored to their interests and ambitions. To date, more than 9,000 matches have been made.

YC charges nothing for these services, nor does it take equity. It pays off for the firm by encouraging more, better-equipped startups to apply to its accelerator. At first blush, that seems to be working: 45% of the W22 batch previously went through Startup School. Some of those accepted founders first met via YC’s matching.

Idea

Once founders enter the idea phase, equipped with a business plan, they apply to YC’s accelerator. Odds of acceptance are low, mooted to be between 1.5% and 3%. Those who are admitted traditionally move to California for the three-month duration, with many settling into an apartment building nicknamed the “Y-Scraper.” Covid disrupted this practice, though YC recently noted its next batch will be in-person.

YC invests $125,000 for 7% in equity with a further $375,000 on an uncapped SAFE with a “Most Favored Nation” (MFN) provision. We’ll discuss how terms have evolved and the current implications later.

In exchange for this equity, founders join the next batch and get access to YC’s broader network. As part of the batch, entrepreneurs get access to expert talks and office hours with YC’s partners. For Malcolm-Wiley Floyd, cofounder of Stairs Financial and W22 graduate, direct access to expertise was extremely helpful. “I could feel the trajectory of our business change in those office hours,” he said, citing the value of partners like Michael Seibel.

As it has scaled, YC may not be able to give as much direct attention as it once did. Ekaterina Damer, the founder of Prolific and YC alum, noted that the recent batches had become a little “too transactional.” She added: “Without wanting to step on anyone’s toes, I would say that “deep mentorship” is more useful than relatively shallow mentorship where small amounts of time are allocated to founders.”

By joining YC, entrepreneurs also unlock an extensive network that includes current batchmates and alumnae. Modern Treasury CEO Dimitri Dadimov commented on this point. “The most influential folks on our journey were probably our batchmates and past YC founders…the founders of companies like Duffel, Titan, Rescale, Skip, and others.”

Many connections within the YC community occur on the internal platform, Bookface, which grew out of one of the accelerator’s creations: Hacker News. In 2006, Paul Graham launched Hacker News (then called Startup News) as a way for YC founders to communicate, connect, and ask for help. The following year, it was opened up to the public. Eventually, in 2013, YC formally bifurcated the platform: the external forum retained the Hacker News name while the internal version became Bookface. Today, it acts as a place for YC’s 7,000 founders to connect, ask questions, and learn from one another – a private social network for some of the world’s best entrepreneurs. Many end up partnering or selling their products to one another.

Zach Sims, founder of Codecademy, noted its value:

Bookface is great. Even though many other investors have their own company portals or email lists, Bookface has incredible scale and so almost always has someone solving the same problem you are who can help.

Another YC graduate described it as “the most high-value network I consume.”

YC’s standard programming ends with Demo Day, in which founders present their company to an army of venture capitalists that vie to fund the hottest startups. Though it is engineered to maximize optionality for entrepreneurs, there are downsides to the frenzy Y Combinator creates – namely in that it encourages shotgun marriages between founders and investors.

Demo Day was traditionally where YC’s formal involvement ended. That changed with the launch of “YC Continuity” in 2015, a growth fund managed by Ali Rowghani and Anu Hariharan. Continuity exercises pro-rata rights in all graduating companies up to a value of $300 million and selectively leads later-stage rounds. It has helped YC to better capture the value it creates, allowing the firm to double down into winning businesses with which it has a close relationship. The existence of Continuity has also given YC an incentive to develop programming designed for more mature businesses.

Inflection

Starting in 2018, YC began helping at what might be called the inflection phase – raising a Series A. According to Hariharan, YC helps founders assess their “readiness” for the round, using their expansive data and expertise to gauge product-market fit. Continuity provides detailed resources – including sample decks – and weighs in on term sheets. Beyond exercising its pro-rata, YC does not lead Series A rounds, allowing the market to price their companies.

YC’s “Work at a Startup” program becomes increasingly relevant starting at this phase. Launched in June 2018, WaaS is a platform that makes it easy to apply for a job at a YC portfolio business. Candidates create a single profile to apply for hundreds of open positions.

“The level of candidates is really strong,” one YC graduate remarked. “You have really talented FAANG engineers just upload their resume.” Hariharan shared the impact WaaS has had on portfolio companies. By her account, 75% of the engineers at startups like Brex, WhatNot, and Faire came from the program. An additional recruiting service assists with executive hires.

It’s worth reflecting at this point on the sheer volume of data YC has at its disposal. Here is a non-exhaustive list of extremely useful things that YC knows and most venture firms don’t:

- YC knows who wants to start a company before they have an idea

- YC knows which founders want a cofounder

- YC knows who is open to a new job

Even if a venture firm has some of this information, none possess it at the scale of Y Combinator. It is collecting tens of thousands of profiles of present and future entrepreneurs and operators, their connections, capital relationships, and hiring needs on a continuous basis. As Hariharan said, “I’m not sure any other fund sees the same volume that we do.”

Growth

This data-set helps Continuity assess which businesses to back once they hit their growth phase. Hariharan and Rowghani typically invest $20 million to $100 million into Series B companies and beyond. In some cases, Continuity puts in as much as $200 million to $300 million across rounds in valuations up to $15 billion, per Hariharan.

Continuity only funds YC graduates, with two exceptions: Convoy and Monzo. Hariharan does not expect those anomalies to become more common: “We don’t spend any time outside of YC.” To date, Continuity has made thirty-five investments, including Stripe, OpenSea, Coinbase, Webflow, Ironclad, and Podium.

In addition to investing, Continuity provides two programs for scaling businesses. If YC’s core curriculum is like an undergraduate degree in entrepreneurship, Continuity’s offerings are the Master’s and Ph.D.

The first is geared toward post-Series A businesses and focuses on fortifying product-market fit, increasing programming velocity, and getting ready for a Series B. Founders are “rebatched” for the six-week program, getting a new peer set.

The second is geared toward true growth businesses and centers around the challenge of “scaling as a CEO,” per Hariharan. Founders are taught best practices in performance management, people leadership, and financial planning. One exercise asks entrepreneurs to write a mini S-1 filing. YC leverages its alumni network to bring tactical advice to this group, with Tony Xu from Doordash and Parker Conrad from Rippling joining as speakers. So far, Continuity has run the program twelve times and assists 200 companies a year across the two curricula.

Don't miss our next briefing. Our work is designed to help you understand the most important trends shaping the future, and to capitalize on change. Join 59,000 others today.

Evolution

It’s worth noting that though YC’s product looks coherent today, it is the result of sustained experimentation. Over the years, YC has toyed with different geographies, organizational types, and funding models. Charting a chronology of YC’s most significant launches reveals what tests stuck and which fell by the wayside.

YC China is the most impactful experiment to have shut down. In August 2018, then-President Sam Altman announced he hired Qi Lu to lead YC’s foray into China. The former Baidu COO – someone Altman had tried to recruit for a decade – was tasked with creating a local chapter of YC. The goal was not only to give the accelerator better access to the country’s best startups but to forge connections between Chinese and American technology companies.

A little more than a year later, YC announced it was backing out, with Qi Lu retrofitting the branch into an independent accelerator: MiraclePlus. The organization gave little color on the volte-face, attributing it to the change in the presidency with Geoff Ralston succeeding Altman in May 2019. It may have been that simple. Ralston does appear to have curbed some of the firm’s more speculative urges, following the closure of YC China with the spin-out of YC Research.

Geopolitical happenings are unlikely to have helped. Twenty nineteen saw an escalation of hostilities, with Chinese telecom business Huawei suing the US and Trump raising tariffs, labeling China a currency manipulator, and supporting Hong Kong protesters. Given the success and strength of its core business, YC may have reasonably felt it was not worth the trouble.

Investing: Industrialized venture

Y Combinator has not only evolved the product it offers but the scale and scope of its investments. The accelerator began by supporting ten businesses in the summer of 2005. Today, it backs nearly 400 per program across sectors and countries. President Geoff Ralston noted that “someday, tens of thousands will go through the batch.”

With the help of friend Shree Bhanderi, co-founder of tilli.app, we have analyzed how YC’s investing has changed over time. As this relies on YC’s public data, there may be gaps. Studied together, it nevertheless shows the most important trends around batch size, geographies, sectors, outcomes, and diversity. Further investigation would help understand many of the connections noted. (You can explore the full notebook here.)

Size

YC’s batch size expansion is widely discussed. Critics commonly suggest that as the accelerator has scaled, it has lost some of its value and prestige, evolving from a community garden into venture’s equivalent of a factory farm.

Ralston dismissed that argument, calling it “an invented criticism.” “I love that our batch is getting bigger,” he said, adding, “People that think YC is too big and that’s hurting the network have it precisely backwards.”

He expects YC to fund as many unicorns on a percentage basis as it has in the past.

On average, YC has grown its batches by 20% per year, though it has not been strictly positive. Twenty-twelve saw a 52% decline in startups from the year prior; 2006, 2007, 2011, and 2021 saw leaps of 40%.

If it keeps expanding at its current rate, YC will support nearly 1,400 companies annually by 2025 and close to 3,500 by 2030. To surpass Ralston’s 10,000 marker would require a further six years.

Geography

The best counter to the argument that YC has lost prestige by supporting more companies is that it has also radically expanded its investment scope. Modern Treasury’s Dimitri Dadiomov highlighted this:

One misconception, I think, is that it has grown from ten to fifty to 150 companies that are the same. In my experience, the growth in the count of companies is more tied to YC entering new “territories.”

These “territories,” Dadiomov explained, could refer to sectors – adding coverage for hardware or AI businesses, for example – or geographies. The data indicate that YC has diversified the countries it draws from, though America remains the dominant geography.

Excluding the US from this analysis gives a clearer picture of which geographies have gained prominence over time.

The “other” Americas have established a strong foothold, with South American startups proving popular in recent years. Asian companies, particularly those hailing from India, have also become more prevalent. After the US, India is the second largest recipient, followed by Canada and the United Kingdom. Nigeria has delivered the most African startups.

Africa’s rise is visible in the latest batch, doubling from 3% to 6%. In W22, American companies made up just 49%; up to 2017, they regularly tipped 80%.

We should expect this trend to continue, given the unique value YC can bring to international founders. Though other investors may be able to provide more localized expertise, none can manifest a Silicon Valley network so instantly. Given that available venture funding is concentrated n the U.S., this is extremely valuable. Christian Van Der Henst, cofounder of Latin American startup Platzi, mentioned this point. “Since I started the company outside the US and outside the Bay Area, both the community and program help a lot,” he said.

As you might expect, given the firm’s previous desire to devote more resources to the country, YC has little foothold in China. Eleven startups have come from China, the same number as those from Egypt, Spain, and Denmark. All are much smaller markets.

Sector

A trend towards greater variety is also visible when studying investments by sector. Starting in 2011, fintech companies became a growing percentage of YC’s batches, expanding from about 7% to 24%. Healthcare startups have seen a meaningful uptick over the same period, expanding from 5% to 10%. Consumer startups are in decline, shrinking from 30% to 14%. Crypto is notably absent from the top categories, though some fall under “Unspecified.” To date, YC had funded just eighty-five crypto or web3 businesses, though twenty-four were part of the last batch. YC seems to have a weak grasp on this part of the startup ecosystem at the moment.

Similar variety shows up when looking at leading sub-categories like B2B, fintech, and consumer, though the smaller sample sizes make this less meaningful.

One impact of YC’s geographical and sector diversification is that it has encouraged venture capital firms to consider different startup profiles. Dimitri Dadiomov commented on this subject:

YC is more uniquely effective now for underrepresented geographies, minorities, educational backgrounds…[essentially] founders who would simply have a harder time raising if YC didn’t provide the “stamp” that this is an acceptable thing to invest in. I always think it’s funny when someone says they’re investing in something like “a YC nuclear fusion company” - this from people who would never even meet with a nuclear fusion startup normally, but because it’s a “YC company” it’s all of a sudden a fine thing to invest in.

In essence, the accelerator has the power to shift venture capital’s Overton Window, making new categories and geographies “investable.”

Diversity

Some believe YC is doing an insufficient job on this front when it comes to supporting underrepresented founders. Paul Biggar, founder of CircleCI and Dark, pointed to this as a particular disappointment. “They were looking for Mark Zuckerberg and they found a lot of them,” he said. (Biggar was kicked out of YC’s community last year for sharing a Bookface conversation in which a founder explained how to cut the covid vaccine line.) Ekaterina Damer of Prolific, who noted her Ph.D. in diversity science, emphasized the same issue:

YC could take a much stronger stance on diversity and inclusion by sending clearer signals to historically under-represented, marginalized founders to say: “You are welcome in the tech world. We want you here and we believe in your potential. We’re showing this by committing to D&I and by taking X, Y, Z deliberate actions to make sure you get the same opportunities as white, straight men in tech. And, we’re monitoring our D&I efforts and will course-correct when we’re off-track.”

Over its lifespan, YC has increased the number of startups with underrepresented founders it backs. Before continuing, it’s worth clarifying what that exactly means. We have used the term “underrepresented” to reflect the three categories that YC breaks out data for: women, black, and Latinx founders. YC provides data on a company level rather than a founder level.

In 2010, just one of the sixty-two companies had a black, Latinx, or female cofounder – less than 2%. In the latest batch, nearly 36% met this category.

This rough trend exists when looking at international or US-only startups, though it is more muted in the latter.

Across all three views, it's clear that growth has stalled (and in some cases declined) over the past three and a half years. In 2019, about 35% of startups were co-founded by underrepresented entrepreneurs. So far, in 2022, it's trending at roughly 35.5%. Of the three categories in which YC provides data, black founders are the least common, co-founding 8% of 2022’s companies. Women and Latinx make up about 19% and 13%, respectively.

How does YC compare to the broader venture industry? With a reiteration of the caveat around the firm’s data – and the difficulty in making perfect comparisons across data-sets – YC compares favorably. According to Pitchbook, 2021 saw US companies with at least one female founder collect 17% of all venture funding. (All-female teams received just 2%.) YC’s figure was slightly above 23% for the same year and geography.

Black founders received 1% of total venture capital investment in 2020, according to Accenture. Though the first half of 2021 saw a four-fold increase from the same period the year prior, share remained mostly steady at 1.2%. About 7% of YC’s 2020 US investments were black co-founded, declining to below 6% the following year.

A similar pattern exists for Latinx founders. Though total dollars invested grew considerably between 2020 and 2021, rising from $2.8 billion to $6.8 billion, the market share was reasonably static, improving from 1.7% to 2.1%. YC’s numbers declined over the same period but remained considerably higher, dropping from 13.2% to 10.2%.

The trendline of YC’s diversity efforts is a source of considerable frustration to founders like Ekaterina Damer: “Right now, I’m mostly unhappy about the rate of change: Things are not only changing too slowly, but sometimes we’re going backward again.”

Another frustration is the sense that much more could be done but that YC doesn’t seem motivated to improve. When Biggar brought up the need for greater diversity with senior leadership in 2017, he left feeling disappointed that it didn’t seem to be a priority. “You can’t reform people that don’t want to be reformed,” Biggar said. Its lack of urgency was a major reason Biggar didn’t bring future startups to the firm.

Explicit in Biggar’s criticism is the belief that YC shouldn’t be compared to traditional venture capital on these measures. “We kind of expect it from VCs,” Biggar said, “everyone at YC thinks they’re the good guys.” An intriguing facet of Biggar’s assessment is that it reveals one of the few times where YC’s source of differentiation invites criticism. The firm was founded on the notion that traditional venture capital was broken and needed to be remade by hackers like Graham. In the years since, YC has continued to emphasize that it is not a venture capital firm, but something entirely different, closer to a university. While this provides valuable separation, allowing YC to elevate itself against the field, it may mean it is judged differently. Measure YC against VC as an industry, and it looks pretty good; compare it to an educational institution like Stanford, and it suddenly appears woefully skewed.

YC has taken steps to improve its diversity. Starting in 2014, Jessica Livingston began hosting the Female Founders Conference to support women entrepreneurs. It has since been renamed the Aspiring Founders Forum. The accelerator hosts events to attract participants from Historically Black Colleges and Universities and other underrepresented groups. Anu Hariharan offers weekly office hours for women in engineering. YC only started breaking out underrepresented founder figures in its public database in 2020. That’s something many other firms do not do and suggests a willingness to be assessed and held accountable for its performance.

Outcomes

So far, we’ve examined how the composition of YC’s batches has changed. But how have the companies themselves fared over time?

As you would expect, most mature companies either end up acquired or closing up shop. Among pre-2015 startups, 29% get bought, 40% die, 30% are still active, and 1.4% have gone public. Outcomes vary considerably between sectors, with consumer startups closing at roughly twice the average rate.

So far, 268 YC startups have reached or surpassed a valuation of $150 million, with the time to reach that benchmark declining over time. On this basis, the W16 looks particularly remarkable, with twenty-eight businesses valued above $150 million. Rappi, Daily, Sendbird, Paystack, Outschool, Embark Trucks, Astranis, Tovala, and Podium were all in this batch.

On a sectoral basis, the number of startups past the $150 million mark maps cleanly to total figures. The only obvious outperforming category is fintech: though just 12.2% of YC companies come from that sector, they make up nearly 19% of the high-value group.

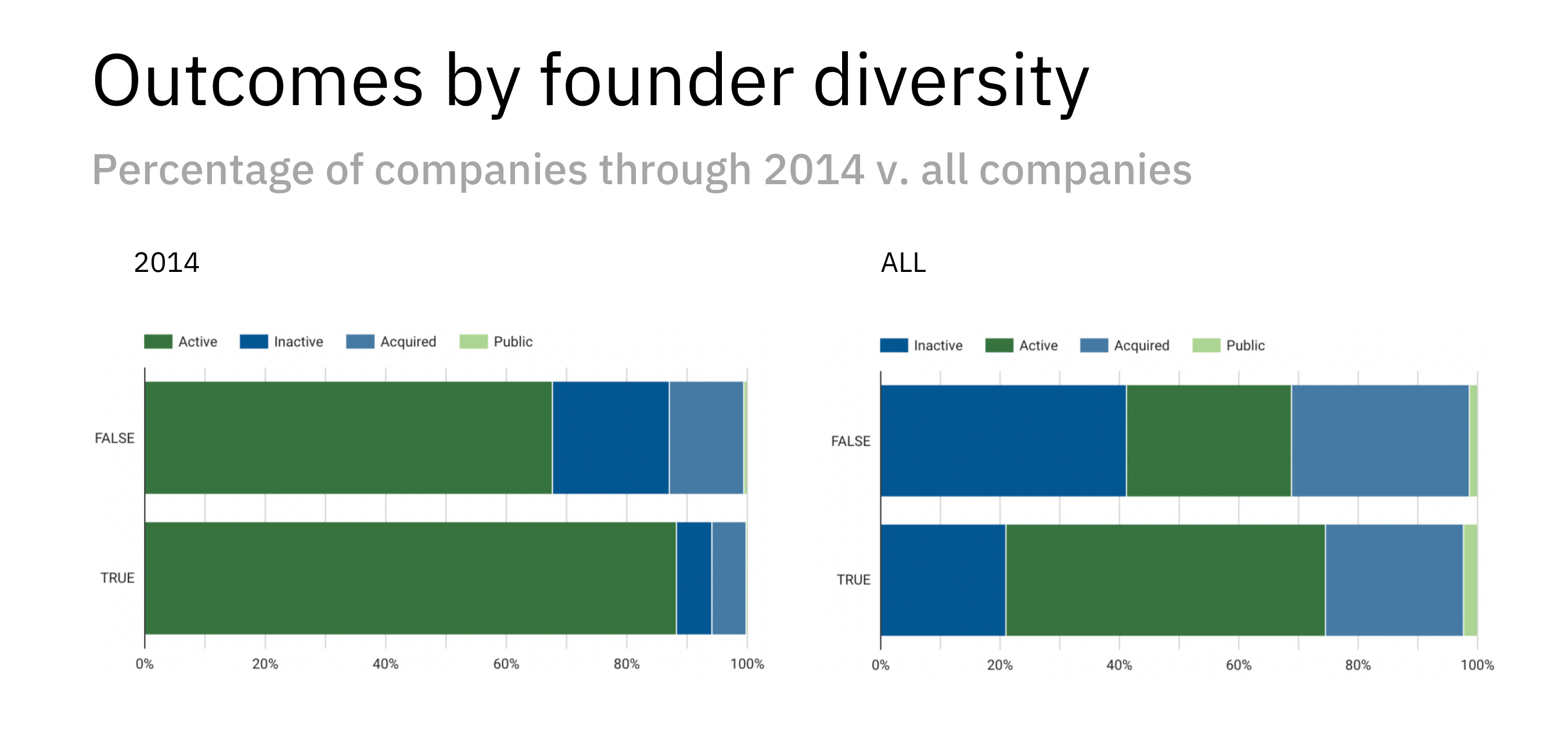

Startups with an underrepresented founder tend to stay alive longer than those without one, though this is partially due to greater diversity in later batches. However, even when looking at startups up to 2014, the trend holds.

The success of underrepresented founders will hopefully give Y Combinator and the broader market reasons to prioritize this segment. “I believe that YC, and all other VCs, could do more to help fix [funding disparities],” Damer noted, “This is not just an ideological position, but an economic one: The potential of minority founders is under-tapped, and the opportunity costs massive. VCs are missing out.”

Terms: Pricing power

In January of this year, former Bolt CEO Ryan Breslow went viral for two Twitter thread critiques of Y Combinator. Breslow referred to the firm, along with Sequoia Capital and Stripe, as one of Silicon Valley’s “mob bosses.”

It’s hard to take Breslow’s depiction of the Grahambino crime family seriously. His argument is a mixture of inaccuracies, insignificances, and contradictions that reads as querulous paranoia. Breslow contends that YC did not fund Bolt because it backed Stripe, an orthogonal rival – never mind that YC is famous for doing exactly that, often backing direct competitors in the same batch. Breslow suggests Hacker News nuked Bolt’s posts in favor of Stripe – as if ranking on the forum might have any meaningful, enduring impact on the success of a venture-backed startup. Breslow contends that YC is near-omnipotent, capable of crushing any who threaten their business, but also not worth the equity it takes. Peppered in are pitches to buy Breslow’s book about fundraising and sign up for news about his upcoming incubator.

Valuations

Tucked away in Breslow’s criticism is one point worth discussing. Are YC’s terms fair? Or are they “beyond predatory,” as the Bolt CEO argues?

When YC first began, it invested $20,000 for roughly 6% of a business. In 2011, the firm upped its stake to 7% for $100,000. Since then, the initial investment has hovered between $120,000 and $150,000 for 7%. As mentioned earlier, the most recent version invests $125,000 with a further $375,000 on an uncapped SAFE with a “Most Favored Nation” provision. The implied valuation of YC startups has grown from roughly $333,000 to a high of $2.1 million before settling at $1.8 million.

Compared to the broader venture market, YC’s terms look extremely expensive. Data collected by Cendana Capital, a fund of funds, shows median pre-seed and seed valuations between 2012 and 2021. Though YC does accept more mature businesses, its batches map best to the pre-seed stage. In 2012, the median pre-seed valuation was $2.8 million post-money, while the median seed was $7.6 million. By 2021, pre-seed valuations had increased to $6 million, and seed valuations passed $15 million. Of course, valuations will vary by geography and sector. Cendana’s data is based on its portfolio, which has international scope but a stronger US presence.

From this vantage, YC’s terms are remarkable. How is the accelerator able to invest in high-potential startups at an 88-70% discount to the median? And how has it managed to sustain this over time? On a relative basis, YC’s terms have actually become more expensive over the past ten years, even as the venture market has grown more competitive. In 2012, YC’s $100,000 for 7% deal represented an 81% discount from median seed valuations and 49% from pre-seed prices.

While in some cases YC invests in startups others might not, by and large, it backs teams capable of raising financing elsewhere, often on much better financial terms. The fact that so many strong entrepreneurs still attend is a testament to YC’s insane pricing power. No other fund on earth is able to invest in so many good founders, so reliably, at such a discount from the market.

Does that mean YC’s terms are predatory? If they are, someone has forgotten to tell the founders. Even detractors like Biggar call the terms “totally fine,” adding, “[YC was] worth it when it wasn’t a kingmaker. It’s certainly worth it now.”

Founders noted that YC’s prestige helps with hiring, landing customers, and collaborating with external partners. “When we went to talk to banks we were ‘a YC company’,” Dimitri Dadiomov said, “At least there was a little more reason to talk to us.” Malcolm-Wiley Floyd of Stairs Financial remarked, “As we start ramping up recruiting for Stairs we want to communicate to folks that they’re making a good decision for their career, adding, “YC definitely helps with that.”

Another reason graduates don’t seem to sweat YC’s steep terms is that Demo Day gives them a quick opportunity to regain any “lost” equity. Having hundreds of venture investors vying to invest inevitably increases a startup’s valuation, making it possible to leave with more money and more equity than you might have otherwise as a median startup. Zach Sims of Codecademy commented on this:

Being a YC company for us helped garner additional press and probably bumped our valuation by 20-30%. I think that’s part of being a YC company, but it’s also part of the feeding frenzy that occurs post-Demo Day when people feel meaningful time pressure to invest in a company.

These dynamics mean YC can be worth it before factoring in the lifetime benefits of an expanded network and continued tutelage through Continuity. One indication that YC earns its equity is the number of founders that return. Though the firm declined to share a precise figure, “hundreds” have reportedly come back one or more times. Many others have circled back to become full-time staff or visiting partners.

Not all will return, of course. Daniel Ha of Disqus hesitated when asked whether he would go back to YC with a future business. “It really depends on the circumstances,” he said, “If I was to start a company as a first-time founder, absolutely.” Naturally, more experienced and better-networked founders may find they’re able to get more generous terms elsewhere.

New deal

YC’s new standard deal is worth discussing in greater detail. From its inception, YC has treated other VC firms as a necessary evil. Though the firm has good relationships with many, including some frequent funders who receive special access to the batch, there is a fundamental distrust for those in the asset class.

YC’s revised terms look like a kind of confrontation. Because founders now receive $500,000 upfront (with $375,000 converting in the next round), they have significantly more leverage than previously. In the past, it was a viable strategy for pre-seed funds to approach incoming YC companies and offer to invest a few hundred thousand dollars. This was attractive for investors as it usually meant capitalizing a company at a discount relative to what it would receive on Demo Day; it was attractive to founders as it gave them more runway and meant they didn’t have to scramble for a sub-par deal at the program’s end. YC’s new terms wipe out this tactic. Now, the firm itself absorbs the interstitial equity opportunity and gives its companies an upper hand in later negotiations. It is brutal and brilliant.

One final question we might ask when it comes to YC’s terms: where does the money come from? While YC’s success means it may partially rely on recycled capital, other funding is necessary. At its current pace, YC is on track to deploy $400 million per year.

Geoff Ralson declined to name any LPs, though he did note that the firm had “permanent capital.” Given its prior involvement, it wouldn’t be surprising if Sequoia Capital were involved. One would also expect endowments, philanthropic institutions, and perhaps even sovereign wealth funds to have contributed.

Sign up to learn about the next generation of disruptors. Every Sunday, we unpack the trends, businesses, and leaders shaping the future. Join us today.

Risks: Watch the throne

YC illustrated that company formation could be standardized – and that it’s a good business. Since it debuted, others have joined the fray, offering different forms of acceleration and incubation. Though this variation means competition isn’t always head-to-head, other programs almost invariably overlap with YC in some respect.

At the same time, YC has issues it should address on the homefront. Let’s walk through both external and internal threats.

External threats

Techstars launched the year after YC, Seedcamp followed in 2007, and 500 Startups opened its doors in 2010. Entrepreneur First (EF) launched in 2011, focusing on matching cofounders. Cofounder Matt Clifford summarized the firm’s approach:

We think you should start a company with a stranger. When we look around the world and ask, “Why aren’t there more great companies?”, we think the obvious answer is: because many of the world’s best potential founders don’t have a world-class cofounder in their personal network.

This approach has worked well for EF, with Clifford noting the portfolio’s value is “$10 billion and counting.” By building around this stage of the entrepreneurial process – and creating a strong European presence – EF has upstreamed YC with some success. In addition to giving a stipend to the entrepreneurs it accepts, EF invests between $54,000 and $98,500 for 10% equity. Precise terms vary across the firm’s six international locations.

Hyper is another interesting insurgent. Launched in mid-2021, the accelerator is associated with Product Hunt and leverages the platform’s distribution to help its portfolio find customers. Hyper seems to focus its efforts on more mature businesses, citing an interest in seed and Series A startups. Given the community Product Hunt already has at its disposal, it wouldn’t be surprising to see Hyper create a version of Bookface, though it would need to figure out how to split internal and external information as YC did between Hacker News and Bookface.

Pioneer is founded by a former YC partner, Daniel Gross, and follows an especially radical program. Anyone can sign up to compete in Pioneer’s global tournament. By making progress, companies rise up a leaderboard. Those that flourish receive an offer from Pioneer: 1% of their company to attend a remote-first incubator, or 2% with a further $20,000 in funding. Pioneer’s structure is designed to support and capitalize upon a distributed base of overlooked and under-networked founders. In that respect, it resembles YC’s Startup School, albeit with a more peer-to-peer approach.

Traditional venture firms have demonstrated an interest in the accelerator game over the past few years. In 2019, Sequoia introduced Surge, a program for startups in India and Southeast Asia. Surge invests $1.5 million into ten to forty companies per year, split across two batches. Earlier this year, the firm announced another variation on this theme: Arc. Along with a seven-week program, founders receive $1 million. The first Arc batch focused on Europe though Sequoia notes a North American version will arrive in a few months.

A16z is trying something similar. START invests $1 million into startups but seems to take a more casual approach when it comes to programming. Accepted founders receive mentorship but don’t seem to be part of a structured cohort.

Do Sequoia and a16z really want to run an accelerator? One source suggested it was unlikely. Running batches like YC – even on a smaller scale – takes time and considerable coordination. According to this individual, efforts like Arc and START are likely intended to show entrepreneurs that no business is too early to talk to the likes of Sequoia and a16z. Providing structured investment terms, the promise of mentorship and the urgency of a deadline may simply help widen the top of the funnel.

Internal threats

YC’s biggest threat may be itself. Though it seems to have scaled smoothly thus far, growing too quickly could diminish the core value. Venture capital is a services business and one-on-one time with partners and experts is perhaps the most impactful thing the incubator has to offer. Can it sustain the caliber of its mentorship as it adds more partners? Can it ensure each new batch member gets as much attention as the last? Though founders can help each other and rely on Bookface’s broader network, losing this would take something fundamental from YC.

YC may also want to update its image. Though Breslow’s polemics had little substance, the response they received suggests that many feel some animosity toward the accelerator. What started as a scrappy, underdog operation is now an industry frontrunner and has attracted the flack that comes with that position. It may not help itself with an attitude that some consider elitist. As it edges toward its twentieth anniversary, the organization may wish to embrace a humbler tone that reflects the relentless drive for self-improvement the organization exhibits.

Few organizations have had a greater positive impact than Y Combinator since the turn of the millennium. Not all will agree with that assessment, given the criticisms mentioned above. But if you believe that progress depends on innovation and entrepreneurship, YC’s significance is manifestly clear.

It has played a pivotal role in 7,000 entrepreneurs getting their start. The businesses it has backed have changed how we travel, learn, play, transport goods, move money, and cure ailments. There’s a good chance that sometime today, you’ll interact with a company that YC helped, whether that’s accessing a file on Dropbox, ordering groceries on Instacart, watching a stream on Twitch, buying crypto on Coinbase, or getting paid via Gusto.

Perhaps even more importantly, YC has changed how the act of business building is perceived. It is no longer insane for a new college graduate to try and start a company of their own; indeed, it’s fashionable. That shift owes much to YC and the curriculum it has helped popularize. Even operators that did not attend the accelerator have benefited from lessons like “do things that don’t scale.”

This is not to say that YC is perfect or cannot be improved upon. Though it compares favorably to the venture market, stagnating percentages of underrepresented founders merit more attention and action. So does the bubbling animosity that effervesces when critics take to Twitter. Its quest to scale sometimes sits at odds with its promise of expert mentorship. If YC can address these issues, it may enter its third decade not only adored by those it has helped but better-appreciated by those it has not.

It’s hard not to feel optimistic. Products like Startup School, Work for a Startup, and cofounder matching are still in their infancy. Continuity’s growth programming remains much newer than YC’s core program. In ten years, each of these individual elements may have expanded and sharpened, adding even more strength to YC’s formidable arsenal.

Though older than many venture capital firms, the accelerator prefers to think of itself as a form of higher education. Measured against universities hundreds of years in the making, Y Combinator’s legacy is just beginning.

The Generalist’s work is provided for informational purposes only and should not be construed as legal, business, investment, or tax advice. You should always do your own research and consult advisors on these subjects. Our work may feature entities in which Generalist Capital, LLC or the author has invested.

Join over 55,000 curious minds.

Join 100,000+ readers and get powerful business analysis delivered straight to your inbox.

No spam. No noise. Unsubscribe any time.